I love how usery is legal. Also love how if you are a bank and have only one dollar in you vaults, you can issue a loan of thirty dollars, out of this air, based on that one dollar

The bank doesn’t even have that money, it’s invented.

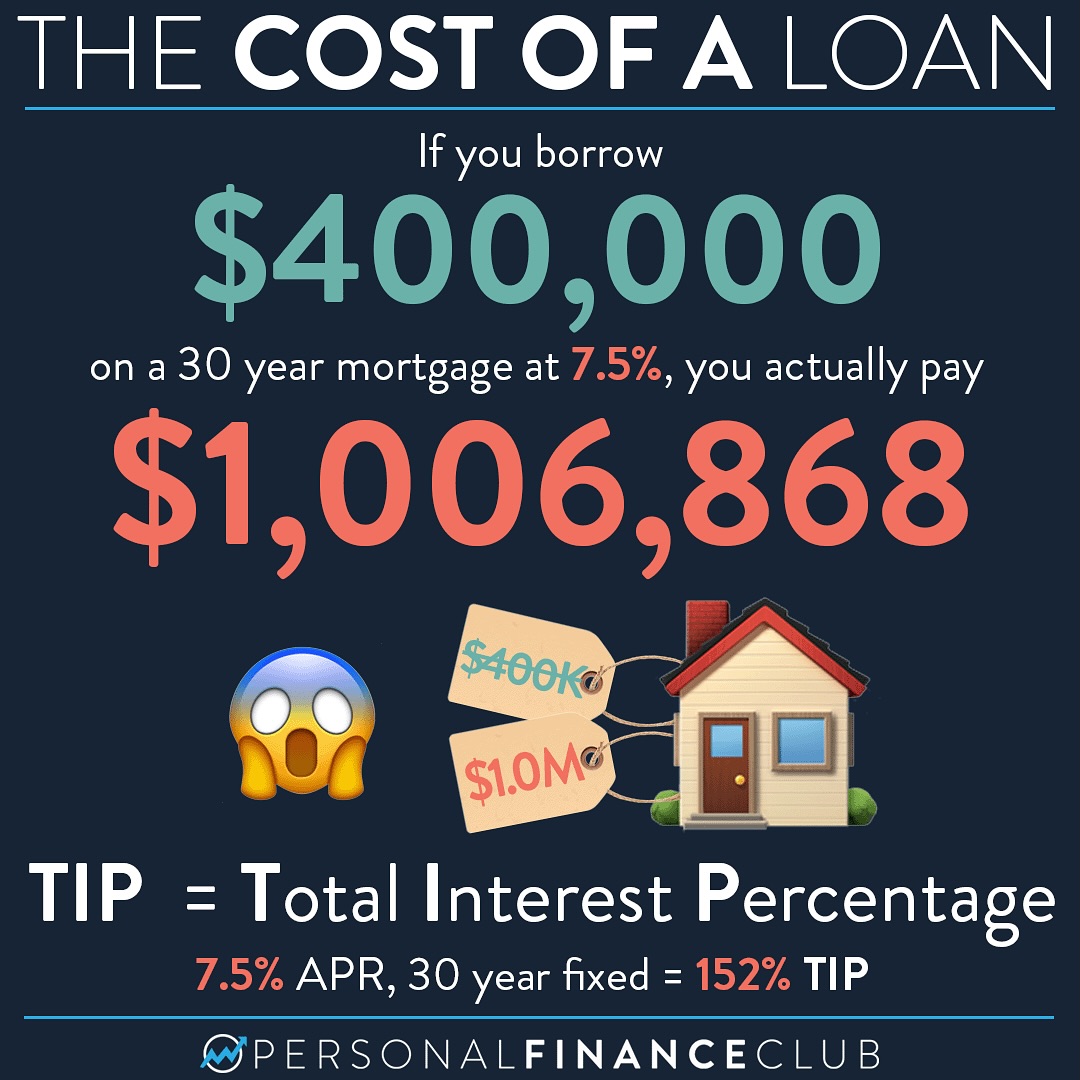

A 7.5% 30 year mortgage is insane, more commonly you will get a 15-20 year 3-5% interest loan depending on the bank and market.

The reason it’s recommended to stay away from 30 year or longer loans, is that you have to deal with the very real threat of inflation for such a long period of time. The purchasing power of $300,000 in 1994 (30 years ago) would be equal to approximately $636,429.08 currently due to inflation. Because of that, the bank has to make good on the massive loss that they’ll take from inflation, causing you to pay significantly more in interest.

All of that still doesn’t mean that banks won’t do everything they can to scalp you of everything you have.

deleted by creator

It’s a horrific market currently, and the 7-9% interest rate range is insane. Thankfully with how interest rates fluctuate, and with it being expected the fed will pull back their inflationary policies in September, it can reasonably be assumed that rates will fall to a much more manageable level by the end of the year or early 2025.

Plus 2019 was a buyers market with very good interest rates in the low 3% range, which imploded further with Covid to record lows of 2%.

With how the housing market is right now, holding off and waiting is definitely the best option. It is the worst possible time to get a fixed rate.

deleted by creator

deleted by creator

were you going for a double negative (won’t do everything they can) in the last sentence

I was, thanks for letting me know!

Yeah, I would rather save to buy a home with cash entirely. What a waste of money.

Assuming you are in a country like the US, the money goes to bank either way. If you aren’t paying a mortgage you are paying rent. The landlord then uses your rent to pay an idenrical mortgage and skim some off the top for themselves.

To decrease total interest cost, here are three strategies:

- Refinance later at a lower interest rate.

- Pay off the mortgage faster than 30 years.

- Buy a more modest place to live, if possible.

Obviously none if that is easy and the first two are basically proxies for making more money but to the extent to which you can make choices those are good ones.

PS there is a hidden fourth strategy called workers’ revolution where you take over the banking and real estate sectors and start treating housing like a place to live rather than an investment.

So I did the math on an example 5 bedroom, 2 bath house of $300K (I picked this because I would need a larger home for my disabled mother and my half-brother to move in with me and my spouse), and let’s say the property taxes are $400/month, home insurance is $75/month, the down payment is 20% ($60K), and interest rate on a 30 year loan is 6.5%. Principal and interest would be $1,517/month according to trulia.

1517 + 400 + 75 = 1,992

(1,992 * 12 * 30) + 60,000 = $777,120 total cost including property taxes and home insurance.

Let’s try 10 years, and let’s give it an interest rate of 5.5%. Principal and interest would be $2,605/month.

2,605 + 400 + 75 = 3080

(3080 * 12 * 10) + 60,000 = $429,600 total cost including property taxes and home insurance.

Let’s instead do a 50% down payment ($150K) on a 30 year loan and a 6.5% interest rate. Principal and interest would be $948/month.

948 + 400 + 75 = 1,423

(1,423 * 12 * 30) + 150,000 = $662,280 total cost including property taxes and home insurance.

Let’s try a 10 year loan and a 5.5% interest rate this time. Principal and interest would be $1,628/month.

1,628 + 400 + 75 = 2,103

(2,103 * 12 * 10) + 150,000 = $402,360 total cost including property taxes and home insurance.

Let’s try the 50% down payment with each but this time with a 2% interest rate. On a 30 year loan, principal and interest would be $554/month.

554 + 400 + 75 = 1,029

(1,029 * 12 * 30) + 150,000 = $520,440 total cost including property taxes and home insurance.

Now let’s try with a 10 year loan. Principal and interest would be $1,380/month.

1,380 + 400 + 75 = 1,855

(1,855 * 12 * 10) + 150,000 = $372,600 total cost including property taxes and home insurance.

Even in the last example, I would consider the additional $72,600 ($15,600 from interest alone) to be pretty high but manageable (to my standards), and this requires being able to afford the enormous monthly cost. I believe the combination of the high principal with the long length of time is the biggest factor in the exorbitant cost in paying interest for the home. Most homeowners don’t earn enough tax deductions to go beyond the standard deduction.

I am very lucky to pay for an 2 bedroom apartment that costs $625/month, rent increase was only $25 every two years, garage is included, and utilities are included except electricity. I have access to great internet from a cooperative. I have been able to get away with having birds as pets with no pet deposits or rent increases (not pet-friendly apartment but received permission from landlord as long as no one complains about the noise). I have been able to screw things in the walls without complaints, and we were allowed to have a garden out in the lawn. I could make do with what I have. If I save for a few years (by reducing my expenses as much as possible), go to college, and earn more to save more, my spouse and I could just save for a home in full without losing so much from interest.

Plus considering dedollarization and the US’s economy potentially collapsing due to politicians’ idiotic policies in the next few or so years, I would rather not be in debt and paying such a high cost for a home per month and struggling because food, gas, household essentials, etc. astronomically increase in price.

The homes that are much cheaper in price and have lower property taxes tend to be in the middle of nowhere with no access to decent paying jobs or even decent internet speeds. Even fixer-uppers and land near better jobs are stupid expensive.

I’m confused about why you’re comparing the cost of a 2 bedroom apartment to a 5 bedroom house. Given that your rent pays someone else’s mortgage plus a bit if graft, the latter will of course be more expensive.

The mortgage of the people you rent from will have the same cost dynamics as you buying a house, more or less. They just pass the cost along to you, with a fee on top so you also help buy them a boat or a vacation or put their kid through college.

I wasn’t mentioning the apartment cost to compare to the house cost, but to mention my house needs given my circumstances and how my relatively low cost apartment plays a factor into my decision to save more for a house first.

Obviously, my landlord benefits from my rent as well as many other people’s greatly. Same as it would for a bank. I have no disagreements with you for the rest of your comment.

In fact, I agreed with your previous comment, too, and I was just highlighting different scenarios to show much over 10 year loans can be very costly. I was trying to demonstrate how the interest rate in combination with the long length of time and high principals make it difficult to avoid the massive interest loss unless every cost cutting tactic is combined. This was to show how saving more for a larger down payment, using a short term loan, and waiting for interest rates to massively decline are all essential to make it possible to own a home. Saving right now is critical.

To clarify, the point was about how my circumstances enable me to save more if I reduce my expenses, and if I were to attempt to save and purchase a home quickly with a low down payment and a 30 year loan with the current insane rates, I would be losing a lot of money. This doesn’t even include inflation and the costs of utilities and expensive home repairs and maintenance, which on top of the astronomical monthly bills makes owning a home not financially feasible for me.

If I were to save longer, inflation would cut out how much I save on interest compared to how much I pay in interest if I paid for a home sooner. Thus there’s probably a middle ground that would be optimal for me to jump into the housing market when saving any longer would make me pay more for inflated home prices.

I picked a 5 bedroom home because, oddly, a similar existing home was actually cheaper than some 4 bedroom or less homes around, which cost $400K+ for some reason. I could probably make do with 3-4 bedroom home.

One issue I face is that homes I see online are dwindling, so I risk waiting for a home too long before my opportunity is lost, but having a home and still paying high monthly bills could put me in a precarious situation as the US economy worsens. Plus I would have to trust I could keep a job in the long term as in this job market there’s nearly 0 tech jobs available besides senior and manager positions, and any jobs I have applied and interviewed for for the past few years I have not been hired for.

Getting a home sucks, homeowners and aspiring homeowners are screwed over by the banks and capitalist society in general in so many ways, and this is essentially my entire point. Workers need to seize the banking and real estate sectors if we want to see any meaningfully beneficial change.

Ah, I see. Wasn’t meant to be a direct comparison so much as looking at your own options.

The upfront cost of a down payment is the largest hurdle, for sure. None of it is easy or fair, it requires having savings despite capitalism underpaying and overcharging us. There isn’t a trick to it or anything it is also down to whether you have the luck and circumstance.

One thing to consider in your calculations is that your mortgage also builds equity. If you rent and need to move, you lose all of your rent. If you have a mortgage and move or get foreclosed you get a chunk of that money back.

unless you’re filthy rich, both home prices and rent goes up faster than the utility of not paying interest.

{kind=link}