I wasn’t mentioning the apartment cost to compare to the house cost, but to mention my house needs given my circumstances and how my relatively low cost apartment plays a factor into my decision to save more for a house first.

Obviously, my landlord benefits from my rent as well as many other people’s greatly. Same as it would for a bank. I have no disagreements with you for the rest of your comment.

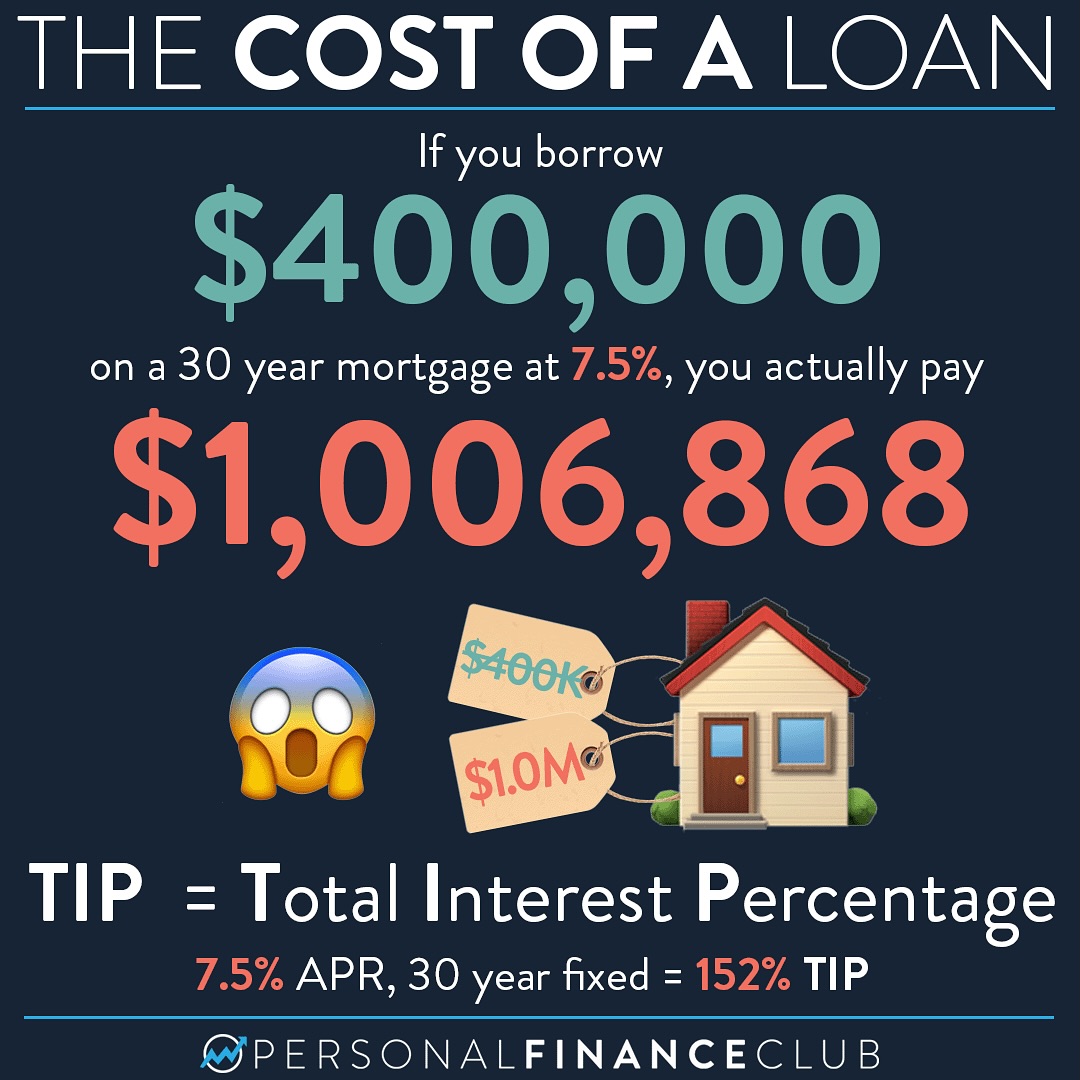

In fact, I agreed with your previous comment, too, and I was just highlighting different scenarios to show much over 10 year loans can be very costly. I was trying to demonstrate how the interest rate in combination with the long length of time and high principals make it difficult to avoid the massive interest loss unless every cost cutting tactic is combined. This was to show how saving more for a larger down payment, using a short term loan, and waiting for interest rates to massively decline are all essential to make it possible to own a home. Saving right now is critical.

To clarify, the point was about how my circumstances enable me to save more if I reduce my expenses, and if I were to attempt to save and purchase a home quickly with a low down payment and a 30 year loan with the current insane rates, I would be losing a lot of money. This doesn’t even include inflation and the costs of utilities and expensive home repairs and maintenance, which on top of the astronomical monthly bills makes owning a home not financially feasible for me.

If I were to save longer, inflation would cut out how much I save on interest compared to how much I pay in interest if I paid for a home sooner. Thus there’s probably a middle ground that would be optimal for me to jump into the housing market when saving any longer would make me pay more for inflated home prices.

I picked a 5 bedroom home because, oddly, a similar existing home was actually cheaper than some 4 bedroom or less homes around, which cost $400K+ for some reason. I could probably make do with 3-4 bedroom home.

One issue I face is that homes I see online are dwindling, so I risk waiting for a home too long before my opportunity is lost, but having a home and still paying high monthly bills could put me in a precarious situation as the US economy worsens. Plus I would have to trust I could keep a job in the long term as in this job market there’s nearly 0 tech jobs available besides senior and manager positions, and any jobs I have applied and interviewed for for the past few years I have not been hired for.

Getting a home sucks, homeowners and aspiring homeowners are screwed over by the banks and capitalist society in general in so many ways, and this is essentially my entire point. Workers need to seize the banking and real estate sectors if we want to see any meaningfully beneficial change.

Ah, I see. Wasn’t meant to be a direct comparison so much as looking at your own options.

The upfront cost of a down payment is the largest hurdle, for sure. None of it is easy or fair, it requires having savings despite capitalism underpaying and overcharging us. There isn’t a trick to it or anything it is also down to whether you have the luck and circumstance.

One thing to consider in your calculations is that your mortgage also builds equity. If you rent and need to move, you lose all of your rent. If you have a mortgage and move or get foreclosed you get a chunk of that money back.

{kind=link}

I wasn’t mentioning the apartment cost to compare to the house cost, but to mention my house needs given my circumstances and how my relatively low cost apartment plays a factor into my decision to save more for a house first.

Obviously, my landlord benefits from my rent as well as many other people’s greatly. Same as it would for a bank. I have no disagreements with you for the rest of your comment.

In fact, I agreed with your previous comment, too, and I was just highlighting different scenarios to show much over 10 year loans can be very costly. I was trying to demonstrate how the interest rate in combination with the long length of time and high principals make it difficult to avoid the massive interest loss unless every cost cutting tactic is combined. This was to show how saving more for a larger down payment, using a short term loan, and waiting for interest rates to massively decline are all essential to make it possible to own a home. Saving right now is critical.

To clarify, the point was about how my circumstances enable me to save more if I reduce my expenses, and if I were to attempt to save and purchase a home quickly with a low down payment and a 30 year loan with the current insane rates, I would be losing a lot of money. This doesn’t even include inflation and the costs of utilities and expensive home repairs and maintenance, which on top of the astronomical monthly bills makes owning a home not financially feasible for me.

If I were to save longer, inflation would cut out how much I save on interest compared to how much I pay in interest if I paid for a home sooner. Thus there’s probably a middle ground that would be optimal for me to jump into the housing market when saving any longer would make me pay more for inflated home prices.

I picked a 5 bedroom home because, oddly, a similar existing home was actually cheaper than some 4 bedroom or less homes around, which cost $400K+ for some reason. I could probably make do with 3-4 bedroom home.

One issue I face is that homes I see online are dwindling, so I risk waiting for a home too long before my opportunity is lost, but having a home and still paying high monthly bills could put me in a precarious situation as the US economy worsens. Plus I would have to trust I could keep a job in the long term as in this job market there’s nearly 0 tech jobs available besides senior and manager positions, and any jobs I have applied and interviewed for for the past few years I have not been hired for.

Getting a home sucks, homeowners and aspiring homeowners are screwed over by the banks and capitalist society in general in so many ways, and this is essentially my entire point. Workers need to seize the banking and real estate sectors if we want to see any meaningfully beneficial change.

Ah, I see. Wasn’t meant to be a direct comparison so much as looking at your own options.

The upfront cost of a down payment is the largest hurdle, for sure. None of it is easy or fair, it requires having savings despite capitalism underpaying and overcharging us. There isn’t a trick to it or anything it is also down to whether you have the luck and circumstance.

One thing to consider in your calculations is that your mortgage also builds equity. If you rent and need to move, you lose all of your rent. If you have a mortgage and move or get foreclosed you get a chunk of that money back.