A summary would be nice.

How would anarchists handle people getting loans to buy expensive things? In an anarchist society/group where they still use regular money

Loans was made to incentivize work under capitalism. There is no need for loans.

Under the current capitalist system, should people who self identify as anarchist, should they not take out loans for houses/cars? Afaik, capitalism would prevent a lot of people from being able to afford to buy a house without a loan.

I don’t think it matters either way. There’s no ethical consumption under capitalism, and we won’t dismantle capitalism by consuming “the right way”.

You didn’t ask about that. You asked about loans under an anarchist society where it isn’t needed.

But under the current capitalist society, I would say take out as little loan as possible. Pay all your debt and work as little as possible to starve the upper class of labour. Use your spare time to organize and help your community.

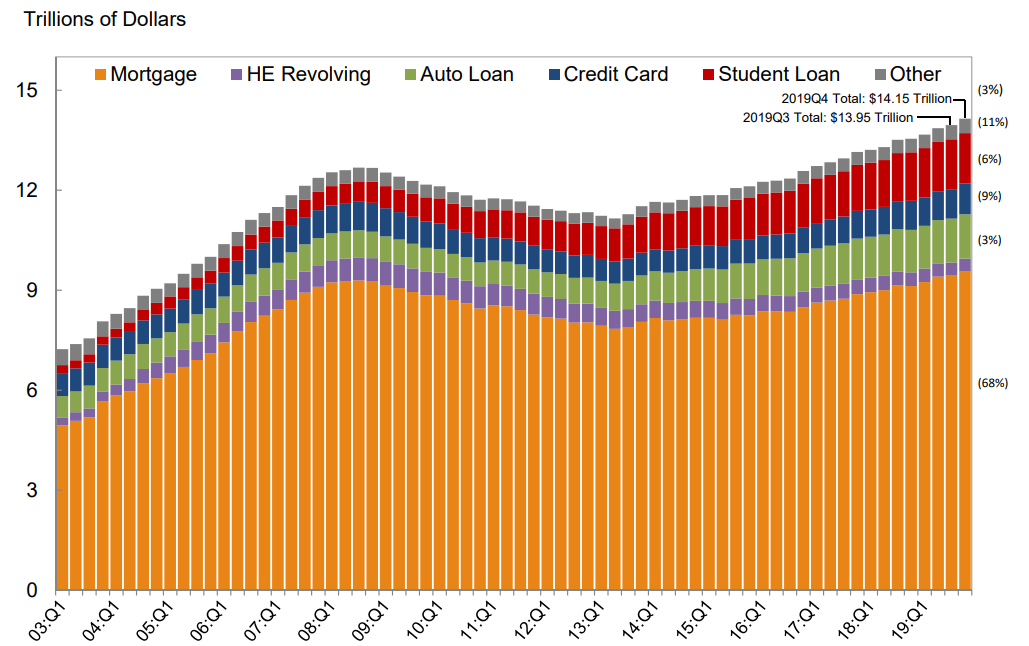

The primary sources of debt in the US is mortgages, at roughly 70% of all outstanding debt. On top of that 10% is a combination of auto and student loans. Already you can eliminate 80% of debt without even touching personal loans or credit card loans used to finance consumption.

Add credit cards to that, you’ve reached roughly 90% of all household debt in the US. The remaining 10% really depends on what it is that one wants to ‘buy’. It’s entirely possible to provide those services without loans.

The thing is, at least under the current system some ones loan is another persons savings (very simplified speaking, no need to lecture me on banks creating loans), thus if you get rid of all the above (which I agree is feasible and desirable) you also need to think of what happens on the other side of the equation (mostly retirement savings). Also doable, but harder.

Well, there is debt and equity. Retirement savings are already largely held in equity and in government bonds. You could argue that some of this is used to finance bank equity and ends up supporting a business model that uses deposits for consumer loans, but that’s a small portion of savings.

Basically, what I’m saying is you can shift most of the debt above to productive investment, rather than to finance consumption of things that should be by right (housing, education, transportation, health care).

afaik anarchism is in favor of housing being a, (whats-the-word) service, rather than a, uh, capitalist good.

Anarchism is in favor of subsidized/free/i’m-not-sure-what-the-word-is education, transporation, health care too?

Transportation as in private vehicle or like buses? Buses i can easily imagine being ‘free’. Private vehicles my imagination isn’t returning anything.

Yes, however mortgages on buildings are often held by institutional investors (managing retirement savings etc.) as they are considered especially safe.

Correct, but the graph above is household mortgages, not commercial buildings. So this debt is indeed originated largely by banks directly to consumers. It is then re-securitized and sold off to more institutional investors who end up holding the debt as an asset, but the liability is on the household side.

what kind of expensive things ?

I was thinking like cars